The Golden Age of the Fifth Techno-Economic Revolution is upon us. In fact, as early as 2017, we had begun our escape from the so-called Great Stagnation which started with the Dot.com crash. But the COVID19 shock has convinced many that mediocrity is here to stay.

Fortunately, Wall Street anticipated the macro-economic trend earlier than Main Street, and this triggered a secular bull market beginning in 2013, which is still going strong. Furthermore, from the vantage point of early 2021, it appears that rather than derailing the Golden Age, 2020’s COVID19 shock simply accelerated the institutional changes needed to facilitate full and effective adoption of Golden Age innovations as they emerge. And, as subscribers to Trends and Business Briefings already know, those innovations in technology and business models are appearing routinely at an ever-accelerating rate.

Consider just one example reported recently by The New York Times. “Artificial intelligence researchers at Google’s DeepMind unit announced that an AI program had solved the mystery of predicting how proteins in the human body fold into 3D shapes. This long-sought breakthrough could accelerate our quest to understand diseases, develop new medi – cines and unlock mysteries of the human body.”

Obviously, finding the solution to this 50-year-old riddle could turn out to be a game-changer for human health and longevity. But more importantly, this advance illustrates why we have legitimate reasons to believe that the long-term slowdown in technological progress is in the process of reversing. And that’s exactly what the Trends editors have been anticipating since the transition began in 2000.

Once that reversal happens, every manager, investor, and consumer needs to be ready for much faster economic growth and all the good things that go with it, such as higher wages and a better quality of life.

To be sure, this forecast boom is not currently expected by from most economists. In fact, all but the most bullish forecasters expect only a growth blip over the next couple of years as the economy rebounds from the pandemic-induced shutdown. That probably means a booming 2021 and 2022 before a deceleration back to an uninspiring pace of around 2 percent, which we’ve been experiencing since the Global Financial Crisis of 2007-to-2009. In fact, the Congressional Budget Office recently predicted that the economy’s average growth potential will be almost a third slower than it has averaged over the past 50 years.

But fortunately, history shows that both the consensus and government studies tend to be wrong more than they are right.

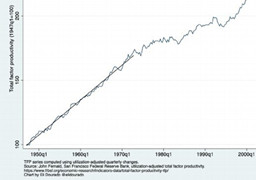

So that begs the question: What would constitute an end to the Great Stagnation and the beginning of a productivity boom? Any precise cutoff will be arbitrary, but a reasonable definition for discussion purposes would be sustained growth in utilization-adjusted total factor productivity of 2 percent per year. For reference, mean average utilization-adjusted TFP growth from 1947 through 1972 was 2.1 percent per year. Since 2005, utilization-adjusted total factor productivity has averaged just 0.17 percent per year.

TFP growth is defined as the change in real output that cannot be attributed to changes in factor inputs like more labor or more capital. And the utilization-adjusted series corrects for the business cycle. So, it’s one of the best metrics we have for measuring the impact of innovation on the economy.

Why did TFP “hit a wall” for most of the past 15 to 20 years? Unfortunately, when it comes to growing TFP, scientific breakthroughs alone are not enough to drive an end to the Great Stagnation. TFP only budges when new technologies are adopted at scale, and generally this means products, not just science. Science lays critical groundwork for new technology, but after all the science is done, much work remains. Someone must shepherd the breakthrough to the product stage, where it can actually affect TFP. This means building businesses, surmounting regulatory obstacles, and scaling-up production.

Traditionally, economic growth is enabled by three factors of production: more capital plus more labor hours worked plus more total function productivity. However, in a landmark study from 2016, Accenture and Frontier Economics concluded that artificial intelligence could be thought of as a distinct factor of production because it combines aspects of the other factors and performs a catalytic function distinct from the others.

As the Trends Editors see it, artificial intelligence is a special form of capital investment, which can substitute for many types of knowledge workers, while enhancing total factor productivity. And while we agree about the distinctive mechanics of AI-based productivity enhancement, we believe that its simply an advanced way to achieve increased TFP.

As highlighted in trend #1, we expect Artificial Intelligence to provide the general-purpose technological boost which will transform gloomy forecasts. Typically, the use case for AI is presented as automating operations such as customer service or improving decision-making through data analysis. Obviously, those solutions are important; that’s why companies spent nearly $50 billion on AI systems last year.

The pandemic has been accelerating that trend. Moody’s Analytics economist Mark Zandi says that many businesses “have taken advantage of the pandemic to more fully deploy technologies and process changes that they were investing in but reluctant to take full advantage of during the good times.”

More important, however, is the role of AI as a “super-researcher.” In a research paper titled “Are Ideas Getting Harder to Find?,” economists Nicholas Bloom, Charles Jones, and John Van Reenen show how it’s been getting harder to discover the big advances and breakthroughs that drive technological progress and economic growth. The low-hanging fruit has been picked. Their conclusion: “Just to sustain constant growth in GDP per person, the United States must double the amount of research effort every 13 years to offset the increased difficulty of finding new ideas.”

But as we’ve documented previously in Trends, artificial intelligence can go a long way toward solving this problem. Instead of thinking of AI as a general-purpose invention, some economists think of it as a general-purpose method of invention that can supercharge the research process. As a result, we believe that, consistent with Accenture’s estimates, artificial intelligence will add two percent per year to average U.S. economic growth through 2035. That, in and of itself, will make all the difference between having a “Roaring Twenties” and a “Boring Twenties.”

Given this trend, we offer the following forecasts for your consideration.

First, by 2035 artificial intelligence will dramatically impact the profitability of almost every industry, but the implications will be far greater for some industries than others.

For example, AI has the potential to increase profits in education by 84%, while in utilities, Accenture estimates the potential profit impact at only 9%.

Second, enabled by AI and super-cheap gene sequencing, widespread commercialization of five nascent medical technologies will dramatically improve the productivity of health care.

The first gamechanger is reprogramming the body to fight back against infectious diseases & cancer using of mRNA. The second is CRISPR gene-editing technology which is finally becoming reliable enough to therapeutically rewrite segments of a patient’s genome, eliminating genetic defects. “In silico drug discovery” will directly harnesses the power of artificial intelligence to the problem of identifying promising therapeutic molecules. Combining these three technologies offers the possibility of slowing and even reversing human aging at some point in the 2020s. And combining AI with the Internet of Things and 5G networking opens the door to low-cost, truly effective telemedicine, anywhere at any time. All of this will combine to “bend the health care cost curve” in ways few expect. The key is ensuring that regulatory constraints don’t undermine the benefits.

Third, telecommuting combined with AI-based self-driving taxis and autonomous delivery vehicles will reduce the share of income households devote to local transportation.

Most families will own just one car or none. Highways will be far less congested despite larger populations and parking garages will be repurposed. Many car-related businesses will become obsolete. And many large metro areas will be served by flying taxis, which will also become autonomous by 2035. The net result will be increased safety, lower costs, and a better experience.

Fourth, space will become a major business destination as launch costs drop by a factor of 200.

Payload launch costs to low-Earth orbit (or LEO) which were $65,400/kg with the space shuttle are now at $2,600/kg for the SpaceX Falcon 9. But now SpaceX is talking about $10/kg with its new Starship. And because Starship is designed to be refuellable in orbit, space planeers will be able to launch 150 tons to LEO, refuel while orbiting Earth, and then fly the same payload the rest of the way to the moons of Jupiter. That’s exciting. But the real impact may be more pedestrian. Meta-analyses have found that trade volume (on Earth) has a roughly inverse-linear relationship to transport costs. If that relationship holds true for space, a 200-times cost reduction in travel between Earth and LEO should increase “trade” between Earth and LEO by 200-times. Commerce between the Earth and the moon, or between the Earth and Mars, starting from a base close to zero, would be stimulated even more. We will have to wait to see exactly what this portends.

Fifth, for the next 20 years, fossil fuels will dominate global energy market, despite the best efforts of environmentalists.

Emerging economies can’t afford the costs and unreliability of today’s renewables. Natural gas will dominate North American electrical production because it’s clean, cheap, and abundant. China and India will rely heavily on coal. However, by the end of the decade, small-scale nuclear energy and advanced geothermal power will both become cost-competitive and will dominate the second half of the 21st Century. Without heavy subsidies, solar and wind will only become competitive for intermittent applications, and only if storage technologies can be substantially improved. Meanwhile, dramatically improved heating and air conditioning technologies, coupled with the transporta tion changes discussed earlier will reduce demand in the advanced economies while making upgrades in emerging markets more affordable. So, barring extreme political pressure, we do not believe energy costs will hinder economic growth in the coming years. And,

Sixth, the biggest impact of artificial intelligence will be in terms of scientific discovery and product development where whole industries will be built around discoveries that could not have even been made without the use of AI.

The protein-folding breakthrough mentioned earlier is only the latest of many blockbuster examples. Back in February, MIT researchers reported that, “A computer model, which can screen more than a hundred million chemical compounds in a matter of days, is designed to pick out potential antibiotics that kill bacteria using different mechanisms than those of existing drugs,” Similarly, Wired magazine reported on InoBat, a Slovakia-based company which is using a U.S.-developed AI platform to analyze different lithium battery chemistries 10 times faster than what was previously possible. And this is just “the tip of the iceberg” when it comes to harnessing the unique abilities of AI to do game-changing scientific research. Since this technology is still in its infancy, the Trends Editors expect to see a whole wave of previously unimagined solutions, which will form the basis for new companies and even new industries.

** Resource List

1. FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES. April 2014. John Fernald. A Quarterly, Utilization-Adjusted Series on Total Factor Productivity.

2. Congress of the United States-CBO. September 2020. Congressional Budget Office. The 2020 Long-Term Budget Outlook.

3. Harnessing AI-Driven Growth.

4. Accenture Institute for High Performance. September 2016. Mark Purdy and Paul Daugherty. Why Artificial Intelligence Is the Future of Growth.

5. Wall Street Journal. December 30, 2019. John McCormick. Businesses Plan to Increase AI Spending. Spending on AI systems is expected to grow 31% in 2020 from 2019, according to IDC.

6. American Economic Review. April 2020. Nicholas Bloom, Charles I. Jones, John Van Reenen, and Michael Webb. Are Ideas Getting Harder to Find?

7. Trends. October 17, 2017. The Trends Editors. AI Transforms the Way We Do Science.

8. National Bureau of Economic Research. March 2018. Iain M. Cockburn, Rebecca Henderson & Scott Stern. The Impact of Artificial Intelligence on Innovation.

9. Review of Economics and Statistics, Volume 90, Issue 1. February 1, 2008. Anne-Célia Disdier and Keith Head. The Puzzling Persistence of the Distance Effect on Bilateral Trade.

10. MIT News. February 20, 2020. Anne Trafton. Artificial intelligence yields new antibiotic.

11. AEIdeas. December 5, 2020. James Pethokoukis. Is the great stagnation over?

이전의 변동 혹은 전이의 시기와 마찬가지로, 기술경제 디지털 혁명의 구축과 전개 국면의 간격은 스태그네이션의 시작으로 특징지어지기도 한다. 이는 닷컴 버블의 경우와도 비슷하다. 그러나 닷컴 버블 이후 우리 세계는 큰 변동을 겪고 성장했다. 앞으로 어떤 세계가 도래할 것인가?

기술경제 디지털 혁명의 황금시대가 성큼 다가왔다. 우리는 사실, 빠르면 2017년부터 닷컴(Dot.com) 충돌로 시작된 소위 대형 스태그네이션(Great Stagnation)에서 탈출하기 시작했다. 그러나 코로나19의 충격으로 많은 사람들은 현재의 상황이 어정쩡한 상황이 되었다고 확신하는 것 같다.

다행히 월스트리트는 일반적인 인식들보다 좀 더 일찍 거시 경제 트렌드를 예상했고, 이것이 2013년부터 장기적 관점의 강세장을 촉발했다. 그리고 이 강세장은 여전히 유효하다. 더욱이 2021년 초의 시점에서 볼 때 2020년의 코로나19 충격은 황금시대를 탈선시키기보다는, 황금시대의 혁신이 등장할 때 완벽하고 효과적인 적용을 촉진하는 데 필요한 제도적 변화를 오히려 가속화한 것으로 보인다. 실제로 코로나19로 인해 기술 및 비즈니스 모델의 혁신들이 일상에서 점점 더 가속화되고 있다. 뉴욕 타임즈에서 최근 보도한 한 사례를 보자.

“구글 딥마인드(Google DeepMind) 사업부의 인공지능 연구자들이 인공지능 프로그램이 인체의 단백질이 3D 형태로 접히는 방식을 예측하는 미스터리를 풀었다고 발표했다. 오랫동안 추구해온 이 혁신적인 돌파구는 질병을 이해하고, 새로운 의학을 개발하고, 인체의 신비를 풀려는 인류의 탐구를 가속화할 수 있다.”

약 50여 년 동안 풀리지 않았던 이 수수께끼에 대한 해법을 찾는 것은 인간의 건강과 장수를 위한 게임 체인저가 될 수 있다. 그러나 더 중요한 것은 이것이 기술 진보에 있어 장기적 둔화가 이제 반전되고 있는 과정에 있다고 믿을 수 있는 확실한 이유를 보여주고 있다는 점이다.

이러한 반전이 일어나면, 모든 기업가와 투자자, 소비자는 훨씬 더 빠른 경제 성장과 그에 수반되는 더 높은 임금 및 더 나은 삶의 질 등 모든 좋은 일을 대비할 필요가 있다.

확실히 이러한 예측은 현재 대부분의 경제학자들로부터 예견된 것이 아니다. 실제로, 가장 낙관적 인 예측가들을 제외한 대부분의 사람들은 팬데믹이 야기한 셧다운으로 인해 경제가 다시 반등하기까지 수년 이상 성장이 멈출 것으로 예상한다. 이는 2%의 시시한 속도로 다시 감속되기 전 2021년과 2022년의 반짝 붐을 의미하는 것 같다. 2007∼2009년의 글로벌 금융 위기 이후 미국이 경험한 일이기도 하다. 사실 미 의회예산국은 최근 평균 경제 성장 잠재력이 지난 50년 동안의 평균보다 약 3분의 1 정도로 둔화될 것이라고 예측했다. 그러나 다행스럽게도 역사는 관련 정부 연구들의 예측과 전망에 틀린 것이 더 많았음을 보여주고 있다. 그래서 이런 질문이 나온다.

‘대형 스태그네이션의 끝과 생산성 붐의 시작은 무엇으로 구성되는가?’

어떤 정확한 컷오프도 임의적일 것이다. 그러나 논의 목표를 위한 합리적 정의는 효율이 조정(utilization-adjusted)된, 연간 2%의 총요소생산성(total factor productivity, TFP)에 있어서의 지속적 성장이다.

미국을 기준으로 1947년부터 1972년까지의 효율 조정 평균 총요소생산성 성장은 연간 2.1%였다. 2005년 이후 효율 조정 총요소생산성은 평균 연간 0.17퍼센트였다. 총요소생산성은 생산량 증가분에서 노동증가에 따른 생산증가분과 자본증가분에 따른 생산증가분을 제외한 생산량 증가분을 의미한다.

이는 정해진 노동, 자본, 원자재 등 ‘눈에 보이는’ 생산요소 외에 기술개발이나 노사관계 경영혁신 같은 ‘눈에 보이지 않는’ 부문이 얼마나 많은 상품을 생산해 내는가를 나타내는 생산효율성지표로, 노동 생산성 뿐만 아니라 노동자의 업무 능력, 자본투자금액, 기술도 등을 복합적으로 반영한 수치로 생산성을 분석하는데 널리 활용되는 지표이기도 하다.

즉, 총요소생산성 성장은 더 많은 노동력이나 더 많은 자본과 같은 요소 투입의 변화에서는 기인할 수 없는 실제 산출물의 변화로 정의된다.

그런데 지난 대부분의 15~20년 동안 총요소생산성이 ‘벽에 부딪혔다’는 이유는 무엇일까?

불행히도 총요소생산성의 성장에 있어 과학적 돌파구만으로는 대형 스태그네이션을 종식시키기에 충분하지 않다. 총요소생산성은 새로운 각종 기술들이 대규모로 채택될 때만 성장하며 일반적으로 이는 단지 과학이 아닌 실질적인 제품을 의미한다.

과학은 신기술의 중요한 토대를 마련하지만 모든 과학이 완료된 후에도 이후 많은 후속 작업이 남아 있다. 누군가가 총요소생산성에 실제로 영향을 미칠 수 있는 제품 단계까지 돌파구를 마련해야하는 것이다. 이는 비즈니스를 구축하고, 규제 장애물을 극복하고, 생산량을 늘리는 것을 의미한다.

전통적으로 경제 성장은 생산의 세 가지 요소, 즉 더 많은 자본과 더 많은 노동 시간, 더 많은 총 기능 생산성(total function productivity)에 의해 가능하다. 그러나 2016년의 획기적인 연구에서 엑센추어(Accenture)와 프론티어 이코노믹스(Frontier Economics)는 인공 지능이 다른 요소의 측면과 결합하고 그 다른 요소와 구별되는 촉매 기능을 수행하기 때문에 생산의 뚜렷한 요소로 고려할 수 있다고 결론지었다.

인공지능은 다양한 유형의 지식 근로자를 대체할 수 있는 특수한 형태의 자본 투자이며 총요소생산성을 대폭 향상시킨다. 즉, 인공지능은 그 기반을 통해 생산성 향상이라는 독특한 메커니즘이며 더불어, 증대된 총요소생산성을 달성하기 위한 진일보된 방법이기도 하다.

앞으로 인공지능은 어두운 예측을 변화시킬 범용 기술들의 향상을 이끌 것으로 기대된다. 일반적으로 인공지능의 이용 사례는 고객 서비스와 같은 운영 자동화 또는 데이터 분석을 통한 의사 결정 개선으로 제시되고 있다. 분명히 이러한 솔루션도 중요하다. 이것이 기업들이 작년에 인공지능 시스템에 거의 500억 달러를 지출한 이유이기도 하다.

팬데믹은 이러한 추세를 가속화시키고 있다. 무디스 애널리틱스(Moody’s Analytics)의 경제학자 마크 잔디(Mark Zandi)는 많은 기업들이 그들이 투자했었던, 그러나 좋은 시기에는 그 수혜를 얻기가 쉽지 않았던 ‘기술’과 ‘프로세스’ 변화를 최대한 활용하기 위해 팬데믹 수혜를 활용하고 있다고 말했다.

그러나 더 중요한 것은 ‘수퍼 연구자’로서 인공지능의 역할이다. 경제학자 니콜라스 블룸(Nicholas Bloom), 찰스 존스(Charles Jones), 존 반 리넨(John Van Reenen)은 ‘아이디어를 찾기가 더 어려워지고 있는가?’라는 제목의 연구 논문에서 기술 발전과 경제 성장을 주도하는 큰 발전과 돌파구의 탄생이 점점 더 어려워지고 있음을 밝혔다. 이들에 따르면 우리는 지금까지 ‘낮게 매달려있는 과일’을 따왔다. 이들의 결론은 이렇다.

“1인당 GDP의 지속적인 성장을 유지하기 위해 미국은 새로운 아이디어를 발굴하는 데 어려움을 겪고 있다. 이를 상쇄하려면 13년마다 연구 노력의 양을 두 배로 늘려야 한다!”

이 부분에서, 인공지능은 문제를 해결하는 데 큰 도움이 될 수 있다. 인공지능을 ‘범용 발명’으로 생각하는 대신 일부 경제학자들은 인공지능을 연구 프로세스를 강화할 수 있는 ‘범용 방법 발명’으로 생각한다. 엑센추어는 인공지능이 2035년까지 미국 평균 경제 성장에 매년 2%를 더할 것이라고 추정하고 있다.

이러한 추세를 고려하여 우리는 향후 다음과 같은 예측을 내릴 수 있을 것이다.

첫째, 2035년까지 인공지능은 거의 모든 산업의 수익성에 극적인 영향을 미칠 것이다. 그리고 일부 산업에는 다른 산업보다 훨씬 더 큰 영향을 미칠 것이다.

예를 들어, 인공지능은 교육산업에서 수익을 84% 증가시킬 수 있다. 반면 액센추어는 유틸리티 산업 분야에서는 잠재적 수익 영향을 9%로 추정하고 있다.

둘째, 인공지능과 초저가 유전자 염기 서열 분석을 통해 5가지 초기 의료 기술의 광범위한 상용화가 의료 산업의 생산성을 크게 향상시킬 것이다.

첫 번째 게임 체인저는 mRNA를 사용하여 전염병 및 암에 맞서 싸우도록 신체를 재프로그래밍하는 것이다. 두 번째는 크리스퍼 유전자 편집 기술로, 마침내 환자의 게놈 부분을 치료 목적으로 재구성하여 유전적 결함을 제거할 수 있을 만큼 신뢰도가 높아질 것이다. 세 번째는 인실리코 신약 발견으로 인공지능의 힘을 유망한 치료 분자를 식별하는 문제에 직접 적용할 것이다. 이 세 가지 기술들이 결합하면 2020년대 어느 시점에서 인간의 노화를 늦추고 되돌릴 가능성도 있다. 그리고 인공지능과 사물 인터넷, 5G 네트워킹이 결합되면 언제 어디서나 저렴하고 효과적인 원격 의료의 문이 열리게 된다. 이 모든 것들이 결합되어 지금까지 거의 예상하지 못한 방식으로 ‘의료비용 곡선을 구부릴’ 것이다. 핵심은 규제 제약인데, 이로 인해 발생할 수혜에 손상이 가지 않아야 한다.

셋째, 인공지능 기반 자율 주행 택시 및 자율 배송 차량과 결합된 원격 근무는 각 가구가 해당 지역의 교통에만 한정되는 비율을 감소시킬 것이다.

대부분의 가구둘이 차를 한 대만 소유하거나 아예 소유하지 않을 것이다. 더 많은 인구에도 불구하고 고속도로는 훨씬 덜 혼잡할 것이고, 주차장은 용도가 변경될 것이다. 수많은 자동차 관련 사업들은 효용을 잃게 될 것이고, 많은 대도시 지역에 비행 택시가 제공 될 것이다. 그리고 이는 모두 2035년까지 완전자율화를 이룰 것이다. 결과적으로 안전성이 향상되고 비용이 절감되며 더 나은 경험이 제공될 것이다.

넷째, 우주 발사 비용이 200배 감소함에 따라 우주는 주요 비즈니스 목적지가 될 것이다.

현재 저 지구 궤도까지의 페이로드 발사 비용은 우주 왕복선으로 kg당 65,400달러이다. 그러나 스페이스X(SpaceX) 팔콘(Falcon)의 경우 kg당 2,600달러이다. 스페이스X는 더 나아가 새로운 우주선으로 kg당 10달러의 목표를 향해 나아가고 있다. 이들의 우주선은 궤도에서 연료를 재충전할 수 있도록 설계되었기 때문에 저 지구 궤도에 150톤을 발사하고 지구 궤도를 돌면서 연료를 보급 받은 후 목성의 달까지 동일한 탑재화물을 옮길 수 있다. 그러나 실제 영향은 거래량에 있다. 메타 분석에 따르면 (지구상의) 거래량은 운송비용과 거의 역선형 관계를 가지고 있다. 이 관계가 우주에 적용된다면 지구와 저 궤도 간의 비용이 200배 감소하면 지구와 저 궤도 간의 ‘거래’가 200배 증가할 것이다. 지구와 달 사이 또는 지구와 화성 사이의 거래에 큰 영향을 미쳐 향후 이 우주 산업 및 비즈니스에는 새로운 지평이 열릴 수 있다.

다섯째, 환경운동가들의 바람과 노력에도 불구하고 향후 20년 동안 화석 연료가 세계 에너지 시장을 장악할 것이다.

신흥 경제국은 오늘날 재생 에너지의 비용과 불안정성을 감당할 수 없다. 천연 가스는 깨끗하고 저렴하며 풍부하기 때문에 북미 전기 생산을 지배할 것이다. 중국과 인도는 여전히 석탄에 크게 의존할 것이다. 그러나 10년이 지나면 소규모 원자력 에너지와 첨단 지열 발전이 모두 비용 경쟁력을 확보할 것이고, 이후 이 에너지가 21세기 후반을 지배하게 될 것이다. 막대한 보조금이 없다면 태양열과 풍력은 간헐적인 응용 분야에서만 경쟁력을 갖추게 될 것이지만, 이도 전력 저장 기술이 크게 향상 될 수 있을 때만 가능하다.

여섯째, 인공지능의 가장 큰 영향은 과학적 발견과 제품 개발이라는 측면에서 인공지능을 사용하지 않고는 불가능했던 발견을 중심으로 산업 전체를 구축할 것이다.

앞서 언급한 단백질 접힘 돌파구는 많은 블록버스터 사례 중 최신 사례일 뿐이다. 지난 2월 MIT 연구진은 ‘수일 만에 1억 개 이상의 화합물을 선별할 수 있는 컴퓨터 모델이 기존 약물과 다른 메커니즘을 사용하여 박테리아를 죽이는 잠재적 항생제를 찾아내기 위해 고안되었다’고 보고했다. 마찬가지로 와이어드 매거진은 슬로바키아에 본사를 둔 회사 이노뱃(InoBat)에 대해 보도했다. 슬로바키아에 기반을 둔 이 회사는 미국에서 개발한 인공지능 플랫폼을 사용하여 이전에 가능했던 것보다 10배 빠른 속도로 다양한 리튬 배터리 화학 물질을 분석하고 있다. 그리고 이것은 획기적인 과학 연구를 수행하기 위해 인공지능의 고유한 능력을 활용하는 것과 관련하여 ‘빙산의 일각’ 불과하다. 이 기술이 초기 단계에서 성숙 단계로 발전하는 경우, 이는 새로운 회사와 새로운 산업의 기반이 될 것이다.

* *

References List :

1. FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES. April 2014. John Fernald. A Quarterly, Utilization-Adjusted Series on Total Factor Productivity.

2. Congress of the United States-CBO. September 2020. Congressional Budget Office. The 2020 Long-Term Budget Outlook.

3. Harnessing AI-Driven Growth.

4. Accenture Institute for High Performance. September 2016. Mark Purdy and Paul Daugherty. Why Artificial Intelligence Is the Future of Growth.

5. Wall Street Journal. December 30, 2019. John McCormick. Businesses Plan to Increase AI Spending. Spending on AI systems is expected to grow 31% in 2020 from 2019, according to IDC.

6. American Economic Review. April 2020. Nicholas Bloom, Charles I. Jones, John Van Reenen, and Michael Webb. Are Ideas Getting Harder to Find?

7. Trends. October 17, 2017. The Trends Editors. AI Transforms the Way We Do Science.

8. National Bureau of Economic Research. March 2018. Iain M. Cockburn, Rebecca Henderson & Scott Stern. The Impact of Artificial Intelligence on Innovation.

9. Review of Economics and Statistics, Volume 90, Issue 1. February 1, 2008. Anne-Célia Disdier and Keith Head. The Puzzling Persistence of the Distance Effect on Bilateral Trade.

10. MIT News. February 20, 2020. Anne Trafton. Artificial intelligence yields new antibiotic.

11. AEIdeas. December 5, 2020. James Pethokoukis. Is the great stagnation over?